FTSE 100 FINISH LINE 7/5/26

FTSE 100 FINISH LINE 7/5/26

London’s FTSE 100 traded lower on Thursday, May 7, as the index struggled to extend the prior U.S.-Iran deal-hopes rally and instead ran into a more difficult mix of weaker oil majors, a stronger pound, political uncertainty and selective earnings reactions. The broader global backdrop was still more constructive than earlier in the week, with investors encouraged by signs that the U.S.-Iran conflict could be moving toward a resolution. But for the FTSE specifically, that peace optimism had mixed effects: it supported global risk appetite and reduced inflation tail risks while also pushing oil prices below 100 and removing support from the index’s heavyweight energy names. The clearest drag came from Shell and BP. Shell fell 2% despite reporting its highest quarterly profit in two years and raising its dividend, while BP lost 1.4% as crude prices retreated. That reaction shows how quickly the market has shifted from rewarding oil exposure to questioning whether the peak in geopolitical risk premia has passed. If a U.S.-Iran deal reduces the probability of a prolonged Middle East supply shock, then the earnings tailwind for oil majors becomes less powerful, even if the companies themselves continue to generate strong cash flow. For the FTSE 100, this matters because energy has been one of the index’s main stabilisers during recent volatility.

The stronger pound added a second headwind. Sterling’s rise against the dollar, driven partly by hopes of U.S.-Iran de-escalation and improved risk sentiment, pressured multinationals that earn a large share of revenues overseas. This is a classic FTSE 100 problem: what looks positive for UK purchasing power and inflation can be negative for the index’s translated earnings base. A firmer pound also complicates the equity reaction to falling oil. Lower energy prices may help consumers and the Bank of England’s inflation outlook, but if sterling rises at the same time, the overseas earnings translation hit can weigh on many of London’s global large caps. Defence also weakened as the geopolitical risk premium faded. BAE Systems dropped 3%, becoming one of the larger contributors to the FTSE’s decline despite maintaining its full-year forecast. The move was less about operational disappointment and more about positioning: as investors price a better chance of Middle East de-escalation, some of the urgency premium that had supported defence stocks is being unwound. That reinforces the day’s central theme — the FTSE was not selling off because the macro news was uniformly bad, but because several of the sectors that had benefited from conflict risk were being de-rated as peace hopes improved.

The domestic political backdrop made the session more fragile. The upcoming elections represent a meaningful test for Prime Minister Keir Starmer’s Labour Party, with the risk that a poor showing could raise doubts about his authority and accelerate discussion of a shift away from Britain’s traditional two-party structure. Markets are not yet pricing a direct leadership crisis, but they are sensitive to anything that could weaken policy clarity at a time when the UK is already dealing with higher building-cost inflation, energy-price volatility and questions over consumer demand. The latest jump in builders’ cost inflation in April is particularly uncomfortable because it keeps pressure on margins and housing affordability, even as lower oil offers some relief elsewhere. Builders are reporting a sharp month-to-month increase in cost inflation, sterling strength is tightening conditions for exporters, and earnings season is revealing an uneven consumer backdrop. That leaves investors reluctant to extrapolate one day of geopolitical optimism into a full UK macro recovery. The BoE may get some comfort from oil below 100, but it still has to weigh domestic price pressures and the risk that confidence remains fragile.

The finish line: Thursday’s FTSE 100 decline was best understood as a rotation away from conflict beneficiaries, not a rejection of global peace optimism. Hopes of a U.S.-Iran resolution helped global sentiment and strengthened sterling, but they also hit oil majors, reduced the defence premium and exposed the FTSE’s sensitivity to overseas earnings translation.

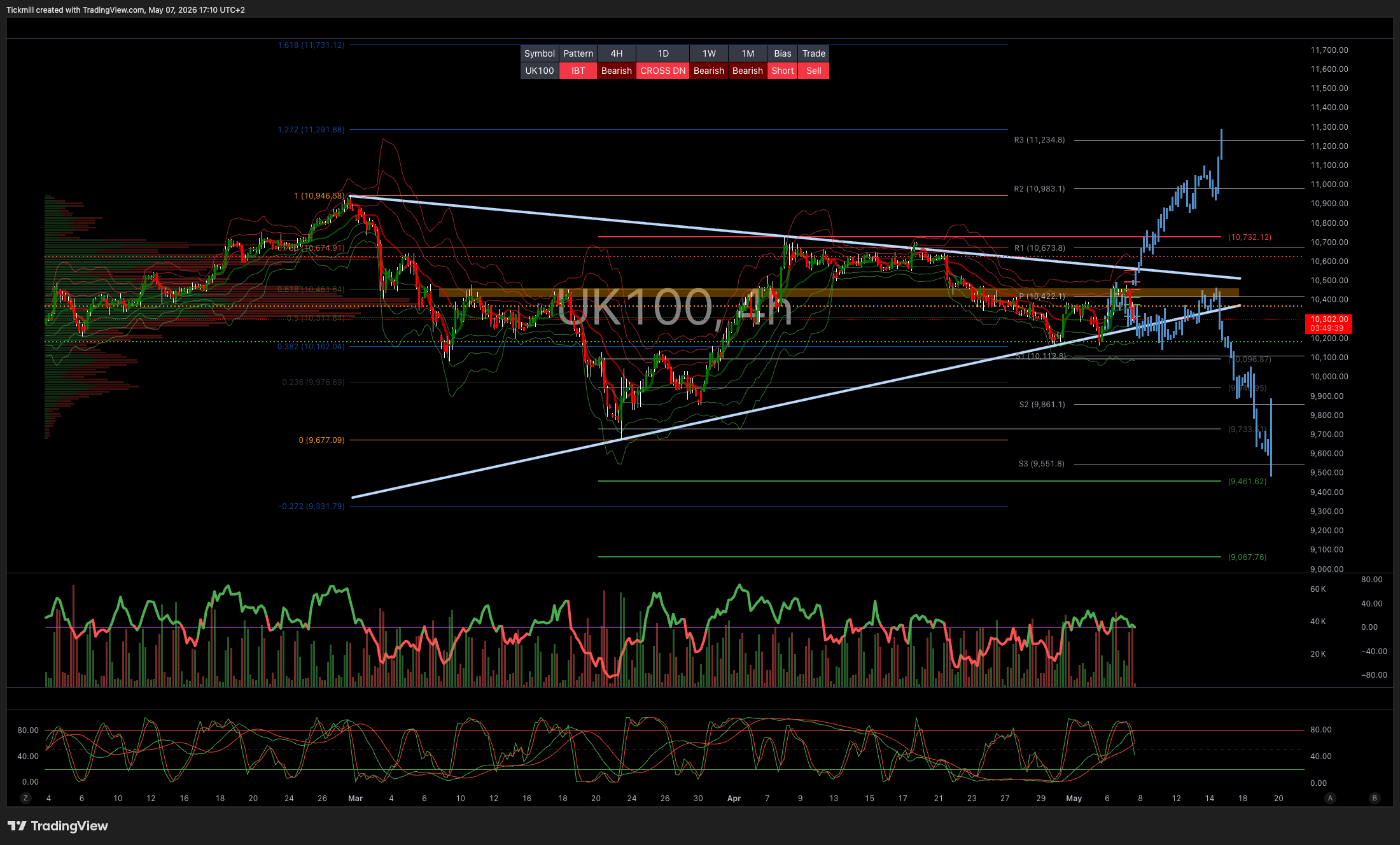

TECHNICAL & TRADE VIEW – FTSE100

Daily VWAP Bearish

Weekly VWAP Bearish

Above 10500 Target 11000

Below 10100 Target 9469

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!